Advertisement

Most Indians discover their health insurance’s real limits only when they’re in a hospital. Two scenarios show exactly where common plans fall short.

Scenario 1: The OPD Bill Your Policy Ignores

Priya visits a specialist, gets blood tests, picks up medication. Total: ₹4,200. Her ₹5 lakh corporate plan pays: ₹0. Standard plans exclude outpatient consultations, diagnostics, and pharmacy unless she’s admitted for 24+ hours. Her cover sat untouched while she paid from her pocket.

Scenario 2: The ICU That Still Cost ₹1.24 Lakh Out-of-Pocket

Rajesh is admitted after a heart attack. Total bill: ₹4.2 lakh. His sum insured: ₹5 lakh. He still paid ₹1.24 lakh personally. His policy had a room rent sub-limit that capped rent at ₹10,000/day, but the ICU cost ₹12,000. Exceeding the cap triggered a proportional cut on his entire bill — surgeon fees, medicines, everything. A 20% copayment clause added ₹84,000 straight from his pocket on a ₹4.2 lakh claim. Consumables like syringes, IV sets, and PPE, worth ₹38,000, were not covered. Furthermore, ₹22,000 in cardiology tests done 35 days before admission fell outside his policy’s 30-day pre-hospitalisation window.

None of this was an edge case. These are standard features of budget health plans. The gaps are predictable — and avoidable.

How Indian Insurers Process Claims

Claims go one of two routes: cashless, where the insurer pays the network hospital directly, or reimbursement, where you pay and then claim. Day-care procedures — cataract surgery, dialysis, chemotherapy — are covered without an overnight stay, but only if they appear on the insurer’s approved list. For a full breakdown of how hospitalisation and day-care claims are processed — including what triggers fast approvals and what causes rejections — read about how health insurance works in India guide.

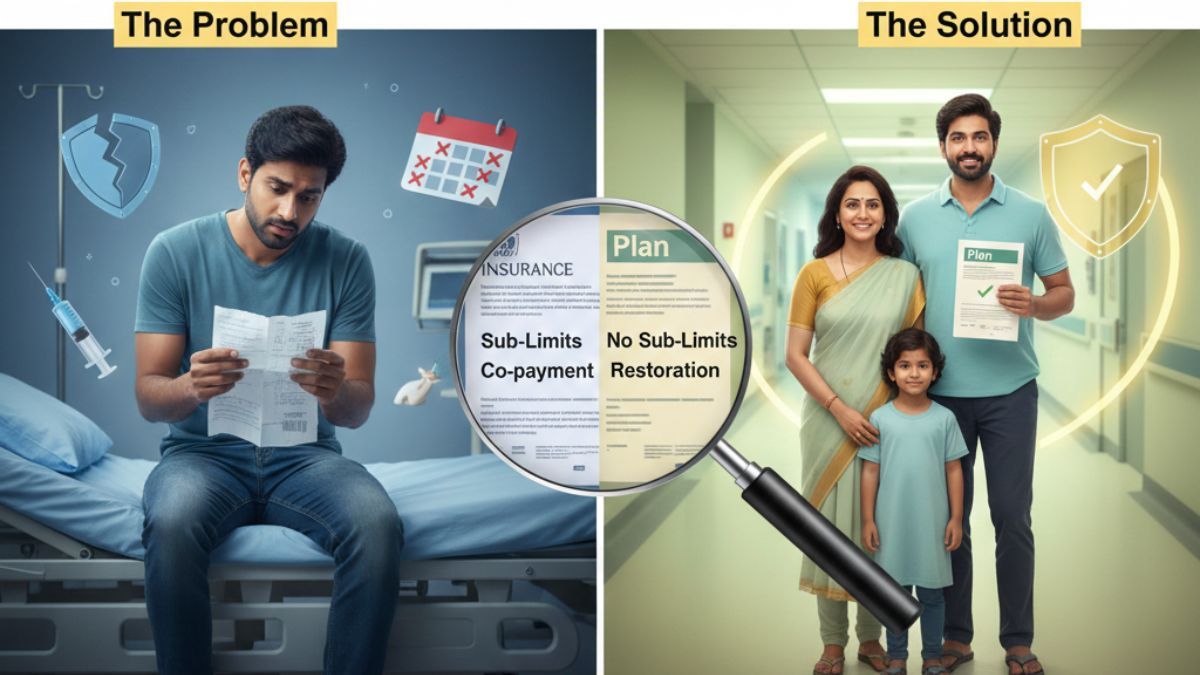

What to Check Before You Buy

The difference between Rajesh’s plan and one that would have covered him fully comes down to five things. First, ensure there are no room rent sub-limits, which would put a single private room at risk of a proportional deduction. Second, look for a policy with no copayment clause, or one capped at a maximum of 20% for senior plans. Third, confirm that consumables are covered, either as standard or through an add-on rider. Fourth, verify the pre and post-hospitalisation coverage is at least 60 days pre and 180 days post (the minimum acceptable is 30 + 90). Finally, look for a restoration benefit, which refills your cover if it is exhausted mid-year.

To avoid surprises at claim time, tick off items like sub-limits, consumables cover, restoration benefits, and pre and post-hospitalisation days against every policy you consider. The full health insurance checklist walks you through must-haves, red flags, and the features most buyers overlook.

The Right Plan Exists — You Just Have to Read the Fine Print

Priya’s OPD gap and Rajesh’s ICU shortfall were both entirely preventable. The plans that work in a crisis share a predictable profile: adequate sum insured (₹10–15 lakh minimum for metro families), no hidden sub-limits, and clear claims processes. The plans that fail do so predictably too. Know which you’re buying before you need to find out the hard way.

Published by Algates Insurance for educational purposes. Not personalised insurance advice. Always read the policy document before purchasing.